Become an Independent Property Claims Adjuster

WORK WITH JEREMY

"CLAIM DADDY" RETTIG

DO NOT PROCEED until you've watched this video.

Join the Best

Join Jeremy "Claim Daddy" Rettig and his community of top-earning adjusters, backed by real-world case studies, one-on-one coaching, and our exclusive 2X Guarantee. Applications are reviewed on a rolling basis and spots are limited—don’t wait.

Submit your application now and start your transformation into a high-income independent insurance claims adjuster!

ACCEPTANCE

requires

application approval

Acceptance is contingent on approval of your application.

What you need to know

About Freelance Claims Adjusting

Skill &

Training

Income &

Potential

Logistics &

Work life

Skepticism &

Trust

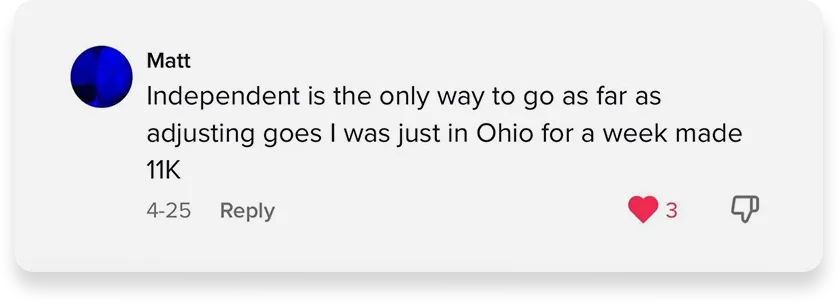

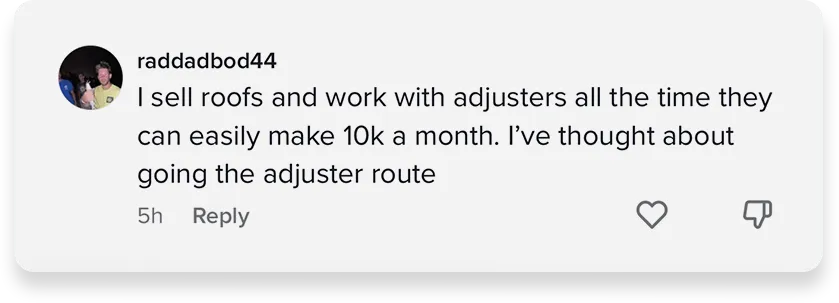

...and it's catching on!

Here's what people have to say..

Facts & Figures

Based on the most recent studies and surveys

1 of 20

Homes in the United States will open a homeowners claim every year.

Verified Source: MoneyGeek

What They Mean for Freelance Adjusters

How those Facts & Figures equates to money in your wallet.

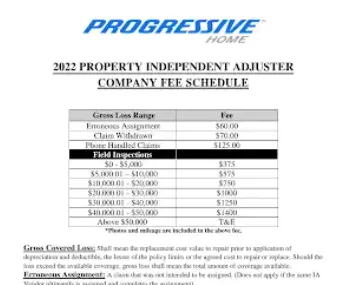

PROGRESSIVE Fee Schedule

$750 Paid to Vendor

Subject to 40% Service (IA) Fee

Paid to YOU.

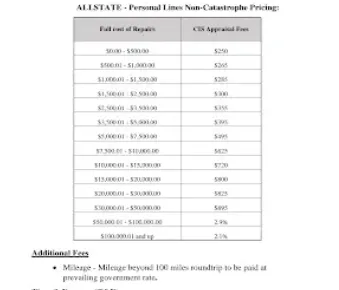

ALLSTATE Fee Schedule

$720 Paid to Vendor

Subject to 40% Service (IA) Fee

Paid to YOU.

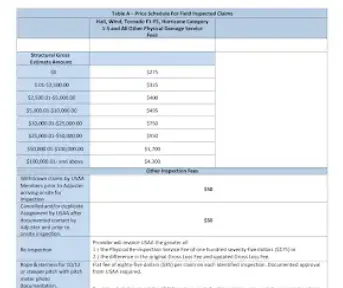

USAA Fee Schedule

$750 Paid to Vendor

Subject to 40% Service (IA) Fee

Paid to YOU.

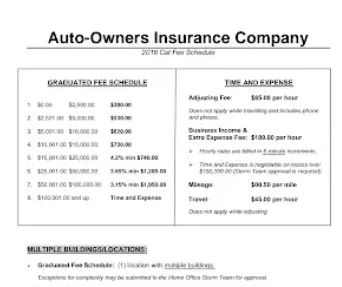

AUTO-OWNERS Fee Schedule

$730 Paid to Vendor

Subject to 40% Service (IA) Fee

Paid to YOU.

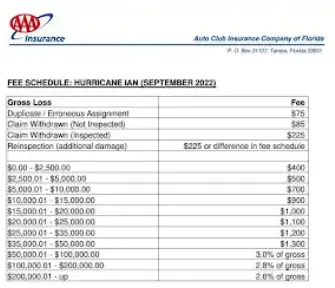

AAA INSURANCE Fee Schedule

$900 Paid to Vendor

Subject to 40% Service (IA) Fee

Paid to YOU.

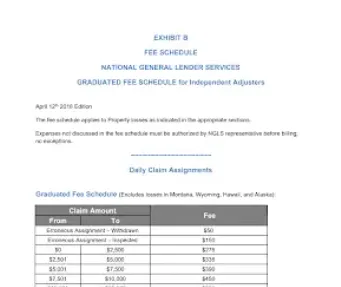

NATION GENERAL Fee Schedule

$550 Paid to Vendor

Subject to 40% Service (IA) Fee

Paid to YOU.

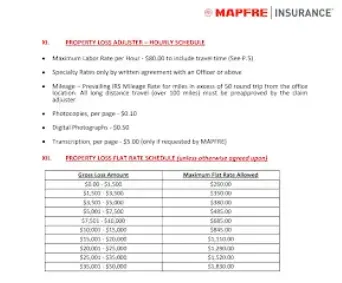

MAPFRE Fee Schedule

$845 Paid to Vendor

Subject to 40% Service (IA) Fee

Paid to YOU.

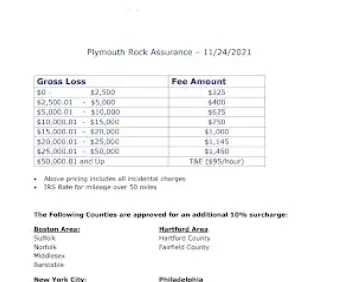

PLYMOUTH ROCK Fee Schedule

$750 Paid to Vendor

Subject to 40% Service (IA) Fee

Paid to YOU.

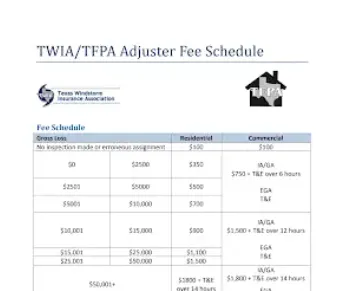

TWIA Fee Schedule

$900 Paid to Vendor

Subject to 40% Service (IA) Fee

Paid to YOU.

These are from Google. Don't believe us? Look for yourself.

ENROLLMENT IS

APPLICATION ONLY

Because of our growing popularity, access to our high-level training (“90-Day Accelerator Program”) is reserved for a limited number of applicants.

Everyone is carefully chosen through a qualification process.

STILL NOT SURE About adjusting?

Frequently Asked Questions

Here are some of the other commonly asked questions

Is there a real market demand for independent property claims adjusters?

Short Answer: Absolutely—there is consistent and growing demand.

Deeper Explanation & Stats:

According to the U.S. Census Bureau, there are over 150 million housing units in the United States. Insurance industry data suggests that roughly 1 in every 20 homes will file a homeowner’s claim in a single year—translating to about 7.5 million home claims annually.

This figure doesn’t include commercial, business-owner, or renter policies, which add millions more potential claims.

The U.S. experienced 18 separate billion-dollar weather and climate disasters in 2022 (per NOAA), highlighting the cyclical surges in claim volume due to natural catastrophes.

Insurance carriers and independent adjusting firms rely on independent adjusters to handle overflow, catastrophe (CAT) situations, and specialized property claims. They are consistently seeking more qualified individuals as the industry battles talent shortages and an aging workforce.

Key Takeaway: The combination of steady homeowner and commercial claims plus the increased frequency of severe weather events drives a constant demand for skilled independent adjusters.

Do I have (or can I acquire) the right skills and expertise to succeed?

Short Answer: If you don’t have them now, you can learn them. There is no lengthy college degree required.

Deeper Explanation:

Minimal Formal Education Requirement: Most states do not require a four-year degree to become an insurance adjuster, although some form of pre-licensing education or exam prep may be mandated.

Learnable Skills: Adjusting involves understanding policy language, learning property damage assessment, and mastering claims software (e.g., Xactimate). All of these are teachable.

Time Investment: The bigger question is how much time and dedication you’re willing to invest to master the essential skills. Training courses, mentorship programs, and hands-on practice can accelerate your learning curve.

Key Takeaway: You are in full control of acquiring the necessary knowledge. There are robust training resources available, and your success largely hinges on your willingness to learn and practice.

What is my unique value proposition or competitive advantage?

Short Answer: Specialized training and a support network set you apart.

Deeper Explanation:

Beyond the License: A large portion of licensed adjusters are just that—licensed and little else. Many have no real training, mentorship, or ongoing education. They’re “runners in a race wearing flip-flops.”

Advanced Training = Real Advantage: By investing in advanced technical training (e.g., scoping damages accurately, advanced estimating tools, negotiation tactics) and tapping into a professional support community, you’ll be entering the same race “wearing high-performance running shoes.”

Professional Branding: Presenting yourself as a well-trained, resourceful adjuster—one who consistently hits deadlines and handles claims efficiently—will help you stand out.

Key Takeaway: The more specialized and practical your training, the stronger your competitive edge. Being licensed is just the start—continuous learning and networking truly differentiate you.

How much capital and financial runway do I need?

Short Answer: You can bootstrap with a few hundred dollars or invest more for faster, stronger results. It’s flexible.

Deeper Explanation:

Basic Costs: A minimal start-up budget might include:

Pre-licensing course/exam fees (varies by state but often $100–$300 total).

Licensing application fees (again varies by state).

Additional Expenses: If you opt for premium resources (advanced training courses, high-level software, or membership in professional organizations), your upfront cost can climb into the $1,000+ range.

Side-Hustle Friendly: Many new independent adjusters keep their full-time job while they train, build experience, and gradually take on claims—reducing the pressure of going “all in” at once.

Key Takeaway: It’s possible to start lean and scale up. Your overall spend often correlates with how quickly and confidently you can break into the field.

Can I handle the risks and uncertainties?

Short Answer: It depends on your comfort level with a variable return on investment and the drive to see it through.

Deeper Explanation:

Upfront Risk: You might invest a few hundred to a few thousand dollars in licensing, training, or equipment. The “risk” is whether you’ll realize a return on that investment.

Earning Potential: According to the U.S. Bureau of Labor Statistics, the median annual wage for claims adjusters, examiners, and investigators was around $68,000 in 2021. Independent adjusters, however, can exceed that number significantly in catastrophe situations or with high claim volumes, but earnings can fluctuate based on workload and disaster frequency.

Time & Money: The less you invest (in both money and time), the more uncertain your outcomes may be. Comprehensive training programs (especially those guaranteeing certain results) can reduce that uncertainty.

Mindset: Ask yourself if the initial financial outlay will “sting” a year from now. If not, this may be a worthwhile calculated risk.

Key Takeaway: You have to be comfortable with potential fluctuations in workload and earnings. With proper preparation and the right training, many find the upside—and flexible lifestyle—well worth it.

What does my support network look like?

Short Answer: It can be as sparse or robust as you make it, depending on whether you join a training community.

Deeper Explanation:

Going Solo: If you don’t have an existing contact or mentor in the industry, you’ll rely heavily on Google, YouTube, and self-directed learning. This path can work but may be slower and more prone to trial-and-error.

Training Community: Programs like Adjuster University offer a community-first approach, giving you:

Peer Support: Fellow students at various stages in their adjusting journey.

Mentor Access: Instructors and industry professionals who can answer questions in real time.

Networking: More connections often lead to more claim opportunities and better professional growth.

Key Takeaway: A strong support network accelerates learning, provides moral support, and can open doors to job leads or contract gigs.

What are the legal, regulatory, or licensing requirements?

Short Answer: Requirements vary significantly by state—some require an adjuster’s license, some do not. Research your state’s rules.

Deeper Explanation:

State-by-State Licensing: Many states (e.g., Florida, Texas, New York) have rigorous requirements, including a pre-licensing course and a state exam. Others may not require a license for property claims at all.

Designated Home State (DHS): If you reside in a state that doesn’t require an adjuster’s license, you can often designate another state (like Florida or Texas) as your “home state” for licensing and reciprocity.

Reciprocity: Holding a license in one state can sometimes allow you to get licensed in another state without retaking a full exam, depending on reciprocal agreements.

Continuing Education: Licensed adjusters typically must complete periodic continuing education (CE) to maintain and renew their licenses.

Key Takeaway: Compliance isn’t difficult, but it’s critical. Identify your state’s requirements early, study accordingly, and maintain your licensure with the right CE credits.